When buying a home, it’s crucial to ensure a smooth transaction by protecting both the buyer and seller. This is where escrow comes in—a secure process that places money and relevant documents in the hands of a neutral third party until all conditions are met. Depending on the location, an escrow officer might be a lawyer or work for a title company, overseeing the process fairly. After a ratified contract is signed, it’s time to summon an escrow officer, usually recommended by your real estate agent, who often has a relationship with experienced professionals. They manage everything, ensuring that funds and paperwork are handled correctly, making the entire process stress-free.

Key Duties of an Escrow Officer in a Property Transaction

A real estate deal involves multiple steps, and an escrow officer plays a key role in making sure everything runs smoothly. Acting as a referee, they ensure that all contractual obligations between the buyer and seller are met before any monies change hands. For a fee of around $1,000, they handle important paperwork, making sure documents are properly signed and become part of the public record. Additionally, they conduct a title search to confirm that the property has no hidden ownership issues. If you’re looking for tips on how to negotiate on a home during the escrow process, check out this detailed guide.

- Ensures all paperwork is signed and correctly recorded

- Verifies that monies change hands only when terms are met

- Confirms both buyer and seller fulfill contractual obligations

- Conducts a title search to avoid ownership disputes

| Responsibility | Description |

| Ensures all paperwork is signed and correctly recorded | Makes sure all documents are properly signed and become part of the public record. |

| Verifies funds exchange only when terms are met | Prevents financial disputes by ensuring payments occur as per agreement. |

| Confirms contractual obligations | Ensures both buyer and seller fulfill their respective responsibilities. |

| Conducts a title search | Identifies any potential ownership disputes or liens on the property. |

Why a Preliminary Title Report Matters in Home Buying?

Once escrow is opened, the title company provides a preliminary title report, also called a prelim, which is an essential document in the home-buying process. This report verifies the name of the property owner, lists any taxes or liens on the property, and highlights any third-party restrictions, such as public or private easements, like a grant allowing an electricity company to place a pole on the land. At this stage, the title contingency in the contract comes into play, so it’s important to look over the details carefully. If there are surprises, like an unknown lien, the buyer has the right to insist that the seller either settle the claims or agree to a reduced purchase price. To better understand how this fits into your overall home buying experience, explore the proven strategies for successful house hunting.

- Reviews taxes, liens, and third-party restrictions on the property

- Ensures the title contingency is met before completing the contract

- Allows the buyer to insist on resolving claims or a reduced price

“Homeownership is a cornerstone of wealth, providing both financial prosperity and emotional stability.” — Suze Orman

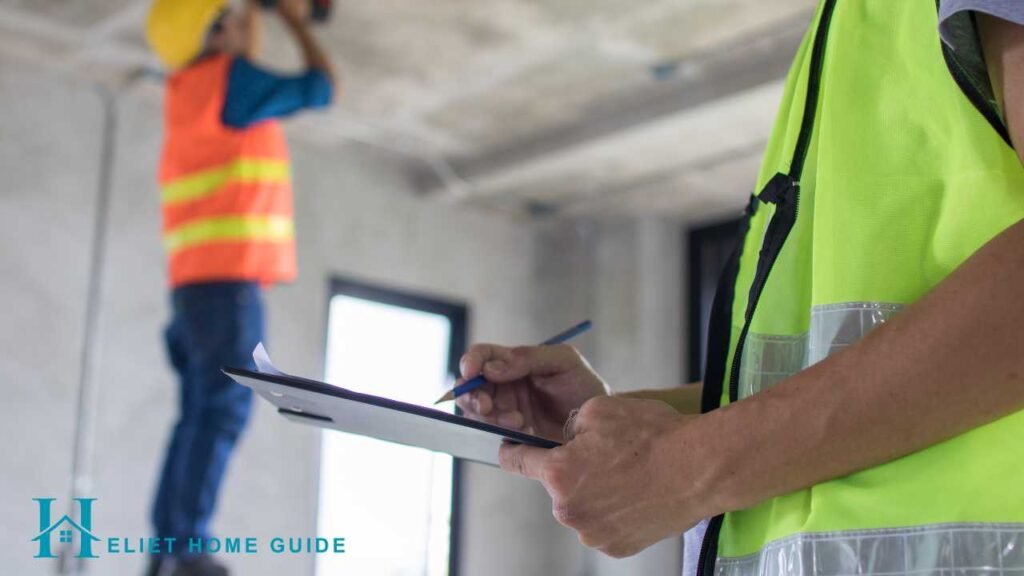

Why a Home Inspection is Essential Before Buying?

Before securing a mortgage, it’s crucial to have the home inspected by a professional to identify any defects or uninsurable conditions. A thorough inspection covers both interior and exterior components, including the foundation, insulation, kitchen, bathroom, plumbing, heating, cooling, electric, walls, roof, and gutters. This process typically takes three hours and costs between $250–500. Additionally, a pest control inspection can detect pest issues or fungal infestation for about $75–150. If you plan to renovate, hiring a general contractor or architect for an estimate on renovation costs can help you budget effectively. The same goes for evaluating a neighborhood; always research steps to evaluating a neighborhood before making an offer.

- A detailed inspection protects both the lender and the buyer from hidden defects

- A pest control inspection prevents costly issues like fungal infestation and pest damage

| Inspection Type | Average Cost ($) |

| Home Inspection | 250 – 500 |

| Pest Control Inspection | 75 – 150 |

How to Choose a Trustworthy Home Inspector?

Choosing an independent inspector is crucial to getting an honest assessment of the property. Avoid selecting someone recommended by your real estate agent, as their interests may not align with yours. Instead of focusing on price, prioritize a quality inspector who can save you money in the long run by identifying hidden issues. Ensure they are a member of the American Society of Home Inspectors and carry errors-and-omissions insurance to cover any mistake they make. A reliable inspector should provide an extensive written report, allow you to be present during the inspection, and offer references from satisfied clients. Similarly, you’ll want to negotiate on a home effectively once issues are discovered during inspection.

- Hire an independent inspector with no connection to your real estate agent

- A quality inspector may cost more but can save you money in the long run

- Ensure they have errors-and-omissions insurance to cover any mistake

- A detailed inspection should include an extensive written report

- Always check references and look for satisfied clients before hiring

“An ounce of prevention is worth a pound of cure.” — Benjamin Franklin

A Comprehensive Home Inspection Checklist

Before closing a home deal, a thorough inspection is crucial to avoid future issues. A professional inspector will check Ceilings, Walls, and Floors for any structural damage. They will examine the Chimney, Fireplaces, and Heating systems to ensure they function properly. The exterior, including Decks, Porches, Balconies, and Siding, will be inspected for stability. Key systems like Cooling systems, Plumbing, Wiring, and Drainage systems must be in good condition. Outdoor areas, such as Walkways, Yard, and Pool, will also be assessed. Finally, elements like Doors, Windows, Stairs, Roof, and Gutters are checked to confirm safety and durability.

| Inspection Area | Key Aspects Checked |

| Ceilings, Walls, and Floors | Structural integrity, cracks, or mold |

| Chimney and Fireplaces | Functionality, ventilation, and safety |

| Heating and Cooling Systems | Efficiency, leaks, and proper operation |

| Exterior (Decks, Porches, Balconies) | Stability, durability, and maintenance |

| Plumbing and Wiring | Proper installation, leaks, and code compliance |

What to Do If a Home Inspection Reveals Issues?

If the inspector finds unexpected problems, the inspection contingency in your contract gives you the right to renegotiate. You can ask the seller to pay for the needed work or agree to lower the purchase price.

Understanding the Importance of Home Appraisal

Before finalizing a property purchase, lenders require prospective home buyers to hire an appraiser to assess its fair market value. This ensures the home is truly worth the agreed price. While some lenders may pay for the service, hiring an independent appraiser offers a more accurate and comprehensive evaluation. The appraisal considers key aspects such as appearance, condition, build quality, and location. Unique features and upgrades can impact the value. A comparison of comparable properties helps determine if the price aligns with the market.

- Lenders require an appraiser to assess the fair market value of the property.

- Some lenders may pay for this service, but hiring an independent appraiser is recommended.

- A comprehensive and accurate appraisal ensures the home is truly worth the price.

- The appraisal considers appearance, condition, build quality, and location.

- Unique features and upgrades can influence the value of the property.

- The value is compared with comparable properties to determine fairness.

- A proper appraisal helps prospective home buyers make informed decisions.

How to Select the Best Homeowner’s Insurance

Buying a home is a big investment, and having homeowner’s insurance is essential to protect both your property and your lender’s investment. A good policy should offer coverage for damage caused by fire, floods, and other disasters. It should also cover loss of personal property—typically 70% of the value—and include liability coverage for personal injury on your property. The monthly insurance payments (or premiums) depend on factors like region, comprehensiveness, and the need for additional riders in areas prone to earthquakes or severe weather. Additionally, when buying a home, consider the steps to evaluating a neighborhood to make sure you’re investing in a location that’s less prone to disasters.

- Guaranteed replacement costs ensure full reconstruction of your home.

- Liability coverage should be at least two times the home’s value for protection.

- Additional riders are necessary for high-risk areas to avoid costly repairs.

| Coverage Type | Key Features |

| Guaranteed Replacement | Ensures full reconstruction of home |

| Liability Coverage | Should be at least two times the home’s value |

| Additional Riders | Necessary for high-risk areas |

“Price is what you pay. Value is what you get.” — Warren Buffett

Key Steps to a Successful Mortgage Application

Getting a mortgage requires a careful application process, even if you are prequalified or preapproved. To speed up the process, have all documents ready, including the final contract signed by both buyer and seller. Lenders will need your Social Security number(s) and addresses from the past two years, including landlords’ names and landlords’ addresses if you were a renter. Proof of income is essential, so provide employer names, employer addresses, W-2 tax forms from the previous two years, and a pay stub showing recent year-to-date earnings. They will also check the balance and monthly payments of loans, charge accounts, and savings, checking, and investment accounts for the last three months. Be prepared with account numbers and any documents like cancelled checks if you receive income from child support or alimony, as it may be relevant to your loan approval. To prepare further, check out these proven strategies for successful house hunting that can help streamline your journey.

- Mortgage approval needs a strong application with complete details.

- Ensure all documents are ready to speed up the process.

- The final contract must be signed by the buyer and seller.

- Provide Social Security number(s) and addresses for the past two years.

- Include landlords’ names and landlords’ addresses if you were a renter.

- Show income proof with W-2 tax forms, pay stub, and year-to-date earnings.

- List all loans, charge accounts, and balances for the last three months.

- Provide savings, checking, and investment account numbers.

- Include documents like cancelled checks for child support or alimony if relevant.

Safeguarding Your Property Ownership and Title

When you buy a property, ensuring a clear title is crucial to avoid legal troubles. Legal ownership of real estate must properly transfer from seller to buyer when a real estate sale happens. However, on rare occasions, errors or fraud can cause issues where the title doesn’t transfer correctly. If such an oversight occurs, the buyer may be responsible for fixing it, even if it wasn’t the buyer’s fault. That’s why lenders and experts recommend title insurance, which protects against unexpected claims. Without it, if things go wrong, you might have to pay large sums to resolve disputes.

Why Title Insurance is Crucial for Homebuyers?

When buying a home, paying a fee of 0.5%–1% of the mortgage value to a title company is a smart move. This company, often acting as an escrow officer, thoroughly researches the title of the property to ensure it’s valid. If their research is wrong and someone makes a claim on the land, the title company will cover the legal costs, protecting your ownership rights.

Ensuring Full Protection with Owner’s Title Insurance

When you buy a home, ensuring you have title insurance that fully protects both you and your lender is important. Many policies focus on the lender’s protection, but once your mortgage is paid off, you may not be necessarily covered. Some states offer bundled policies that include protection for the homeowner, while others require an additional fee of about $30. Always check your policy details to make sure you’re fully covered.

Understanding Different Types of Property Ownership

When a homeowner is taking title, they are transferring legal rights from the seller to the buyer. If buying property alone, the sole owner has full control, but when buying jointly, the co-ownership form must be carefully chosen. Many couples opt for joint tenancy, where both owners share equal rights, and one cannot sell or change ownership without the other’s approval. This option also offers tax breaks if a member dies, allowing the surviving partner to inherit full ownership of the home without legal complications.

Conducting a Final Walkthrough Before Closing

Before closing escrow, buyers get a final walkthrough to ensure their new home is in the expected condition. This is the last chance to inspect the property for any additional damage that may have occurred since the last visit. If any significant issues arise, the verification process allows buyers to renegotiate under the condition contingency. This step ensures that no last-minute problems delay the official transfer of ownership. If you’re in the final stages of home buying, don’t forget to review how to negotiate on a home as part of closing discussions.

The Last Steps in Closing the Escrow Process

- The closing is the final meeting where the buyer, seller, agents, lawyers, and an escrow officer come together to complete the deal.

- In some states, the funds may need to be handed over before the closing, ensuring everything is in place.

- At this stage, the buyer will receive key documents, including the deed of trust, mortgage note, and final sales contract.

- A closing statement is provided, recording all money involved in the transaction, ensuring transparency.

- Once everything is confirmed, the keys to the property are handed over, marking the official transfer of ownership.

How Earnest Money Deposits Work in Escrow?

You mention escrow but don’t explain how an earnest money deposit (a key part of real estate transactions) is held in escrow to demonstrate the buyer’s commitment.

It would be helpful to outline what happens if a buyer backs out—does the seller keep the deposit, or is it refunded?

“The most secure way to double your money is to fold it in half and tuck it into your pocket.” — Kin Hubbard

Important Escrow Deadlines and Timelines You Should Know

- The article explains key escrow steps, but it would be beneficial to include a general timeline of how long each step takes (e.g., typical escrow periods range from 30 to 60 days).

- Buyers and sellers should be aware of deadlines for contingencies like financing, inspection, and appraisal to avoid delays.

What Buyers Need to Know About the Closing Disclosure?

- Before closing, the lender provides a Closing Disclosure (CD), which outlines final loan terms, costs, and monthly payments.

- Buyers should review this carefully to ensure there are no unexpected charges or errors before signing the final documents.

How Escrow Holdbacks Help Resolve Post-Closing Issues?

- Sometimes, issues arise that prevent full closing (e.g., unfinished repairs, incomplete inspections).

- In such cases, an escrow holdback may be arranged, where some funds are held in escrow until the issue is resolved.

- This is important to mention for buyers and sellers to understand their options if last-minute problems arise.

| Closing Step | Description |

| Funds Handed Over | In some states, funds are transferred before closing. |

| Key Documents Received | Buyer gets deed of trust, mortgage note, and final sales contract. |

| Closing Statement Provided | A record of all financial transactions involved. |

| Keys Handed Over | Marks the official transfer of ownership. |

Earnest Money Deposit (EMD) in Escrow:

Once an offer is accepted, the buyer typically deposits earnest money into escrow, ranging from 1% to 3% of the purchase price. This deposit shows the buyer’s good faith in completing the purchase. If the transaction proceeds smoothly, the EMD is applied toward the down payment or closing costs. However, if the buyer backs out for reasons not covered by contingencies, the seller may keep the deposit as compensation for lost time.

Understanding the Closing Disclosure and Final Loan Terms:

Three days before closing, buyers receive the Closing Disclosure (CD), which provides a detailed breakdown of their loan terms, closing costs, and monthly mortgage payments. This is a crucial document that should be reviewed carefully for accuracy. If any discrepancies arise, they should be addressed immediately with the lender to avoid last-minute delays.

Handling Last-Minute Repairs with an Escrow Holdback:

If required repairs or improvements are not completed before closing, an escrow holdback can be used to keep part of the seller’s funds in escrow until the work is finished. This arrangement ensures the buyer is protected while allowing the closing to proceed without unnecessary delays. It is particularly common in transactions involving home renovations, septic system repairs, or weather-related delays.

Common Reasons Escrow Fails and What to Do Next

Not all transactions reach the closing stage. If escrow falls through due to financing issues, inspection problems, or title defects, the purchase agreement may be canceled. The buyer typically receives their deposit back if the issue falls under a contingency. However, if the buyer backs out for an unapproved reason, the seller may be entitled to keep the earnest money. Understanding these scenarios helps buyers and sellers prepare for potential challenges during escrow.

Frequently Asked Question

What is escrow in a real estate transaction?

Escrow is a neutral third-party process where funds and documents are securely held until all conditions of a real estate transaction are met, ensuring fairness for both buyers and sellers.

What does an escrow officer do?

An escrow officer verifies contracts, handles funds, ensures all paperwork is signed, conducts a title search, and facilitates the legal transfer of property ownership between buyers and sellers.

Why is a preliminary title report important?

A preliminary title report verifies property ownership, identifies liens, and highlights restrictions. It ensures a clean title transfer, preventing legal disputes and financial issues for the buyer.

What happens if an inspection reveals major issues?

If an inspection uncovers significant problems, buyers can renegotiate terms, request repairs, or back out under contingency clauses, protecting their investment from costly future repairs.

What is an earnest money deposit (EMD)?

An earnest money deposit is a buyer’s good-faith payment, held in escrow, showing commitment to the purchase. If conditions are met, it’s applied toward closing costs.

How does an appraisal affect closing?

An appraisal determines the home’s fair market value. If the appraisal is lower than the agreed price, buyers may renegotiate, cover the difference, or cancel under appraisal contingencies.

What is the role of the Closing Disclosure?

The Closing Disclosure details final loan terms, interest rates, closing costs, and monthly payments. Buyers must review it three days before closing to ensure accuracy and avoid surprises.

What is an escrow holdback?

An escrow holdback occurs when funds are retained until agreed-upon repairs or conditions are met, ensuring sellers complete obligations before finalizing the transaction.

Can a real estate deal fail during escrow?

Yes, escrow can fail due to financing issues, inspection problems, or title defects. Buyers may recover deposits if covered by contingencies, but sellers may keep them if not.

Why is homeowner’s insurance necessary for closing?

Lenders require homeowner’s insurance to protect against fire, theft, or natural disasters. It safeguards both the buyer and lender’s investment, ensuring financial security.

Conclusion

In conclusion, the home-buying process involves several important steps to ensure a smooth and secure transaction for both the buyer and seller. Key stages such as escrow, home inspections, appraisals, and title searches work together to protect all parties involved, minimizing risks and potential issues.

Understanding the roles of professionals like escrow officers, inspectors, and appraisers, as well as carefully reviewing crucial documents such as the Closing Disclosure, can help buyers make informed decisions. By staying diligent throughout these stages, buyers can safeguard their investment, ensuring a successful and stress-free home purchase.

“Do not wait to buy real estate. Buy real estate and wait.” — Will Rogers

Rhys Henry is a Luxury Realtor & Senior Partner at Tyron Ash International, specializing in South East London & Kent Division. A dedicated real estate agent, Rhys is passionate about helping clients navigate buying, selling, and investing in luxury properties with expert guidance and industry-leading strategies.